PAR Technology: Buy, Sell, or Hold After Q3 Earnings?

PAR Technology’s stock has experienced a significant decline over the past six months, with its value dropping by 42.6% and settling at $35.71 per share. This downturn has left many investors questioning whether this is an opportunity to buy or a risk to avoid.

The question remains: Is PAR Technology a good investment, or should it be avoided? While the lower price may seem appealing, there are several factors that make us cautious about this stock. Here are three key reasons why we believe PAR Technology is not currently an attractive option for investors.

Cash Burn Ignites Concerns

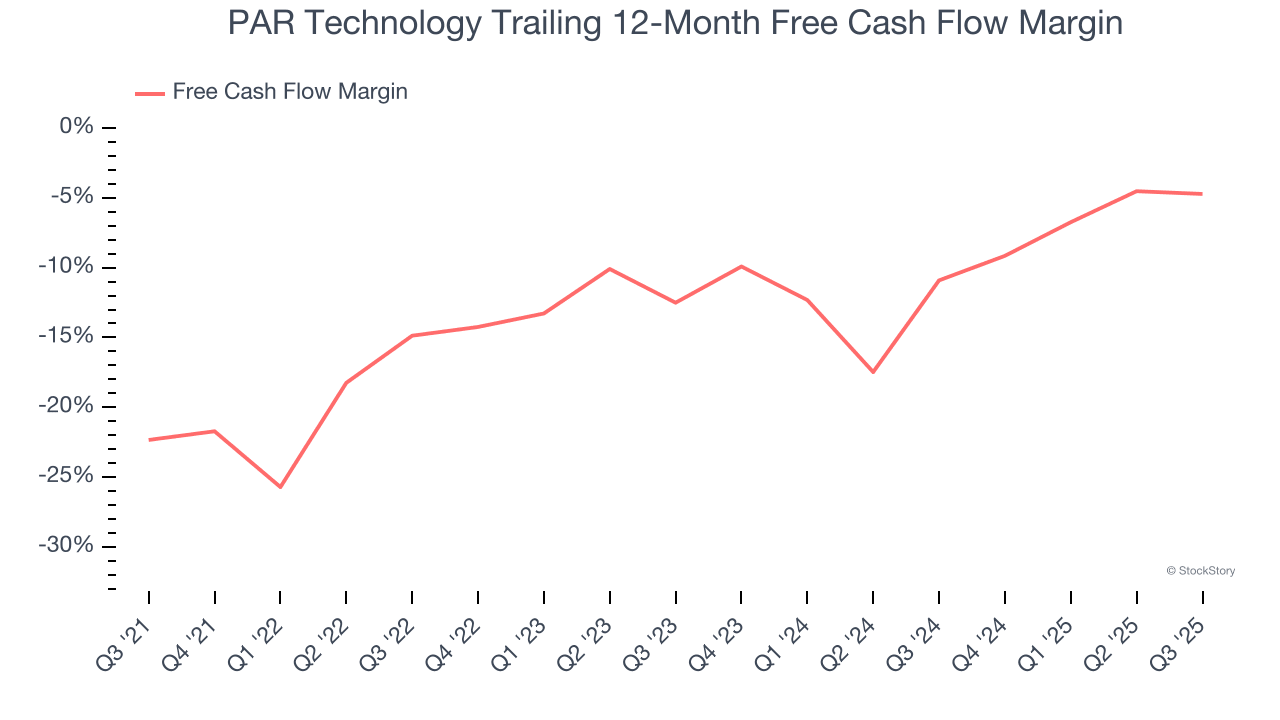

At StockStory, we have always emphasized the importance of free cash flow. Why? Because in the end, cash is essential for a company's survival and growth. Accounting profits alone cannot cover operational expenses or pay dividends.

Although PAR Technology reported positive free cash flow in the most recent quarter, the overall financial picture tells a different story. Over the past five years, the company has been reinvesting heavily, which has drained its resources and limited its ability to return capital to shareholders. Its free cash flow margin averaged a negative 12.2%, meaning that for every $100 in revenue, the company effectively lost $12.16 in cash.

Previous Growth Initiatives Have Lost Money

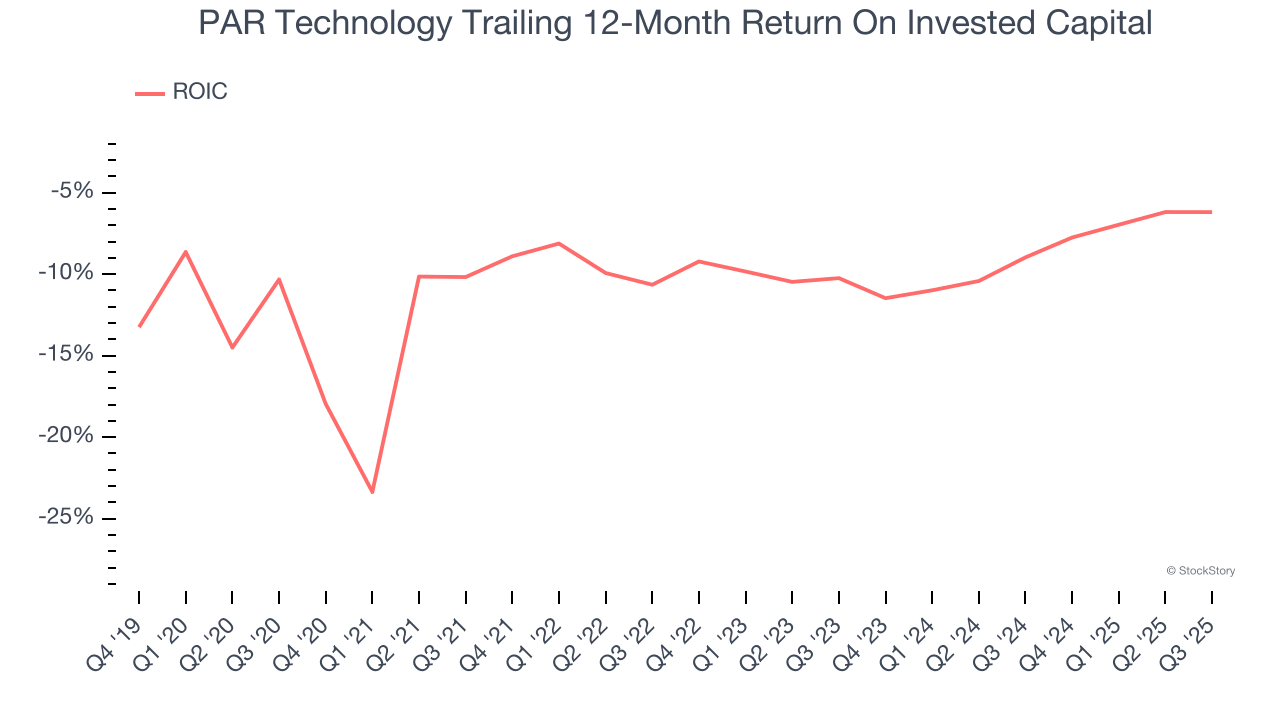

Growth is often seen as a sign of a company's potential, but it’s equally important to assess how efficiently that growth was achieved. One key metric for evaluating this is Return on Invested Capital (ROIC), which measures how much operating profit a company generates relative to the capital it has raised.

PAR Technology’s five-year average ROIC was a negative 9.2%, indicating that the company lost money while attempting to expand. These returns were among the worst in the business services sector, raising concerns about the effectiveness of its growth strategies.

High Debt Levels Increase Risk

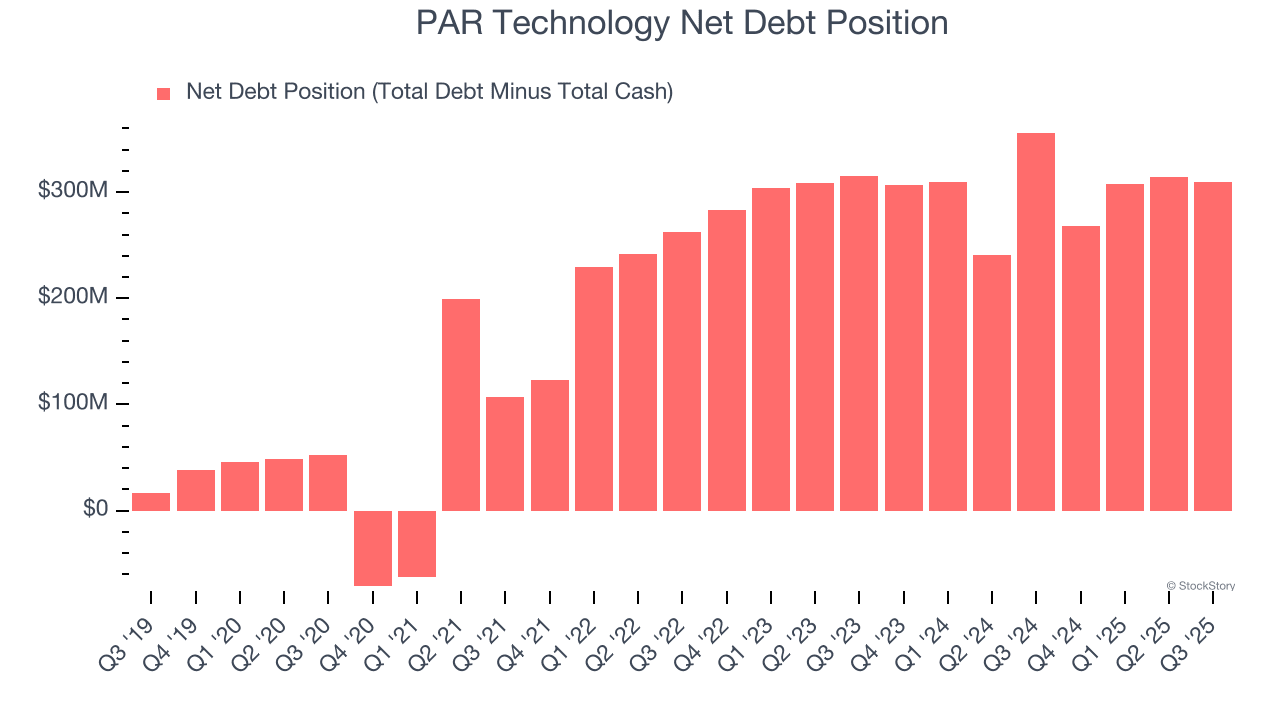

Debt can be a powerful tool when used wisely, but it also comes with risks. As long-term investors, we tend to avoid companies that take on excessive debt because it can lead to insolvency if not managed properly.

PAR Technology has a debt load of $402.3 million, which far exceeds the $93.01 million in cash it holds on its balance sheet. Additionally, its net-debt-to-EBITDA ratio stands at 14×, based on EBITDA of $21.7 million over the last 12 months. This indicates that the company is significantly overleveraged.

At this level of debt, any further borrowing could become increasingly costly, and credit agencies might downgrade the company’s rating if profitability declines. PAR Technology could also face serious challenges if market conditions change unexpectedly—something we aim to avoid when investing in high-quality companies.

We hope that PAR Technology can improve its balance sheet and remain cautious until it can increase its profitability or reduce its debt burden.

Final Judgment

While PAR Technology is not a terrible business, it is not one of our top recommendations. After the recent drop, the stock is trading at 89× forward P/E (or $35.71 per share). Although some may see value here, we don’t currently perceive a major opportunity.

There are certainly more exciting stocks available today. If you're looking for high-quality investments that have delivered strong returns, consider exploring our curated list of market-beating stocks.

Stocks We Would Buy Instead of PAR Technology

Your portfolio shouldn't be built on outdated stories. The risks associated with crowded stocks are increasing daily.

The next wave of high-growth stocks is already here. Our Top 9 Market-Beating Stocks include names that have outperformed the market over the last five years. Some of these stocks have delivered impressive returns, such as Nvidia, which saw a 1,326% increase between June 2020 and June 2025.

Other under-the-radar companies, like Tecnoglass, have also shown remarkable growth, with a 1,754% five-year return. Discover your next big winner with StockStory today.

{kind=link}

Post a Comment for "PAR Technology: Buy, Sell, or Hold After Q3 Earnings?"

Post a Comment