How Debt, Inflation, and Politics Are Raising Borrowing Costs

The Rise in Long-Term Bond Yields and Its Global Implications

A prolonged period of elevated long-term bond yields is significantly increasing borrowing costs across the globe. This trend is primarily driven by investors demanding additional compensation for holding government debt, given the persistent budget deficits, stubborn inflation, and growing concerns about central bank independence.

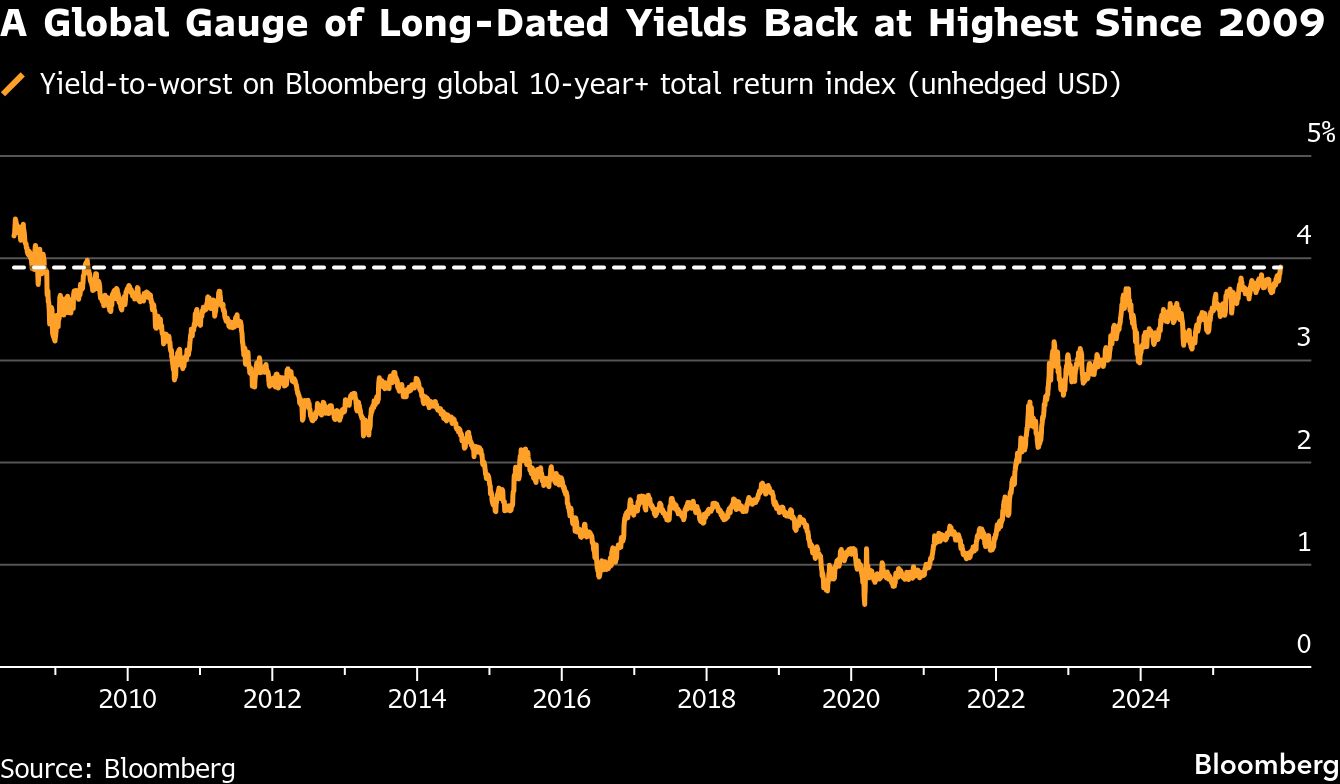

Expectations that a cycle of central bank rate cuts will soon end — and potentially give way to rate increases in certain regions — are also affecting market sentiment. As a result, yields on longer-dated debt have returned to levels not seen since 2009.

As investors evaluate the yields at which they are willing to purchase bonds, they are increasingly concerned about the lack of ambition or capability among politicians to manage their countries’ finances effectively. If rising borrowing costs coincide with sustained price pressures, central banks may find themselves unable to respond effectively.

What’s Been Happening with Long-Dated Bonds?

Traders buy and sell bonds based on the relative appeal of their fixed interest payments. The longer the time until maturity, when the principal investment is repaid, the more potential risks can arise during that period. Notes and bonds due in 10 to 100 years typically offer higher interest rates than short-term bills, as a form of compensation for the added risk.

When a country's economic outlook deteriorates, bond yields usually fall because investors are willing to accept lower returns. This is often in anticipation of central banks shifting their focus from fighting inflation to stimulating economic activity through lower benchmark interest rates. Additionally, the prospect of lower returns from stocks and other economically sensitive assets can boost demand for bonds.

However, recently, yields for long bonds have been on the rise. In the United States, this is partly due to a strong economy that has driven stock prices to record highs, while inflation has remained stronger than expected.

Why Are There Concerns About Debt and Deficits?

Governments around the world took on significant amounts of cheap debt following the 2008 global financial crisis, and then borrowed even more to cope with the economic impacts of the coronavirus lockdowns and recessions. Global debt reached an unprecedented $324 trillion in the first quarter of 2025, according to the Institute of International Finance, with China, France, and Germany being major contributors.

This borrowing spree was fueled by a prolonged period of ultra-low interest rates after the financial crisis, which ended abruptly when the pandemic caused a surge in inflation. Major central banks raised interest rates and reduced their bond-buying programs, known as quantitative easing, making it harder to sustain such high levels of borrowing. Some central banks are now actively selling the debt they accumulated through quantitative easing back into the market, further increasing upward pressure on bond yields.

The concern is that if yields remain high and governments fail to address their fiscal challenges, the cost of servicing some of this debt will continue to climb.

In the U.S., the cost of President Donald Trump’s sweeping tax-and-spending law is another worry for bond investors. The One Big Beautiful Bill Act could add $3.4 trillion to the U.S. deficit over the next decade, according to the Congressional Budget Office. Moody’s Ratings downgraded the U.S. to a lower credit rating in May, citing fears that the growing national debt and deficit will damage its status as a leading destination for global capital.

Import tariffs imposed by the administration in 2025 have generated about $240 billion in revenue through November, helping to narrow the deficit for the fiscal year. However, even if these tariffs survive legal challenges, they won’t be sufficient to close the gap.

What’s Been Driving the Recent Bond Moves?

In addition to ongoing debt challenges, politics have played a major role in recent bond movements.

Donald Trump has repeatedly criticized Federal Reserve Chair Jerome Powell, whose term ends in May 2026, for not cutting interest rates quickly enough. White House National Economic Council Director Kevin Hassett is emerging as a likely successor, and he is widely seen as supportive of Trump’s preference for lower rates. Concerns about the independence of the next Fed chair are prompting some investors to demand higher interest rates as compensation for holding U.S. Treasuries. The assumption is that the next Fed chair might push for faster, deeper rate cuts to please Trump, leading to a surge in inflation and higher bond yields.

The combination of global risks is pushing up what investors demand for the uncertainty of holding bonds for longer — known as “term premia.”

Why Is a Spike in Long Bond Yields a Problem?

Investors prefer the bond market to be predictable and stable, as these assets provide a reliable income stream that balances out the volatility of higher-risk investments like technology stocks.

When longer-term yields rise, it increases the cost of mortgages, auto loans, credit card debt, and other forms of borrowing, putting pressure on households and businesses and weakening economic activity.

If long bond yields remain high, it will gradually increase the cost for governments to borrow as well. That, along with any worsening of the economy, could lead to a “doom loop” where debt levels keep climbing regardless of government actions on taxes and spending.

Historically, market rebellions have even led to the fall of governments, as seen in the UK in 2022. Then-Prime Minister Liz Truss’s mini-budget, which included billions in unfunded commitments, caused turmoil in the bond market and led to increased borrowing costs. In the early 1990s, so-called bond vigilantes were powerful enough to force President Bill Clinton to rein in U.S. debt.

Where Could Things Go From Here?

It remains unclear what a prolonged period of higher borrowing costs would mean for the mountain of long-term debt that governments accumulated during 15 years of ultra-low interest rates. The shift in yields is already leading to new phenomena with unpredictable consequences.

Japan’s government bonds used to have such low yields that they acted as a kind of anchor, exerting downward pressure on global yields. In the UK, Chancellor Rachel Reeves must demonstrate control over the nation’s finances while managing internal party tensions over spending. In the U.S., there are still concerns that post-pandemic inflation is not yet under control, and that Trump’s import tariffs could add further inflationary pressure, exacerbating the bond yield spike. On the other hand, his trade war may weaken the economy, prompting the Fed and other central banks to cut interest rates.

Or both scenarios could occur, resulting in a surge in prices alongside falling economic output — a situation known as stagflation. This would add to the uncertainty over monetary policy, forcing the Fed to choose between supporting growth or suppressing inflation.

Is This a Taste of the Future for Long Bond Yields?

Jamie Rush, Tom Orlik, and Stephanie Flanders of Bloomberg Economics have argued that politics and structural forces could make 10-year Treasury yields of 4.5% the new normal. This comes as decades of decline in the “natural” interest rate — the real interest rate that would prevail if the economy were operating at full employment with stable inflation — have already ended and partially reversed.

“In the years ahead, the natural rate is set to edge higher still,” Rush, Orlik, and Flanders wrote in a book, The Price of Money, published in August 2025. “If risks from debt, climate, geopolitics, and technology crystallize, it could rise quite a lot.”

{kind=link}

Post a Comment for "How Debt, Inflation, and Politics Are Raising Borrowing Costs"

Post a Comment