Alphabet's Unstoppable Rise – Here's the Reason

Key Takeaways

Alphabet's earnings growth is heavily influenced by cloud margins, which are a critical factor in its financial performance. Despite the pressure from AI developments, search and YouTube continue to generate strong cash flows. The company's robust balance sheet and share buybacks offer stability for long-term investors.

Why Alphabet Might Be a Strong Investment Right Now

Alphabet (GOOG) currently appears to be fairly valued in an environment where many tech stocks have high valuations. This is a positive sign. However, there are execution risks to consider. The main question is whether Google Cloud can maintain healthy margins as AI spending increases.

For years, Alphabet relied on search and YouTube for revenue, but recent earnings growth has come primarily from Cloud profitability. This is a significant upside. The risk lies in the potential impact of AI competition on search economics, which could outpace the growth from Cloud.

Search and YouTube remain the primary cash generators for Alphabet, providing the necessary funds for its AI investments and buybacks. However, the durability of these profits is under scrutiny as new AI models change how people search and consume information. The trajectory of Cloud margins is now more important than just revenue growth because of the ongoing disruption on the search platform.

If Cloud margins remain stable, Alphabet's case as a stable compounder becomes stronger.

Google Cloud’s Operating Leverage Is Finally Showing Results

Google Cloud is beginning to show the operating leverage that investors have long awaited. Revenue increased by 32% year over year to approximately USD 13.6 billion. The operating margin reached 20.7% this quarter, a significant improvement from previous years. This shift represents a major change in Alphabet's earnings profile.

The business model is straightforward: sell compute, storage, and AI infrastructure through Google Cloud Platform (GCP), then add higher-value services like data analytics and generative AI. As enterprise clients scale up, fixed costs are spread out, allowing margins to expand faster than revenue. This is classic operating leverage.

The backlog indicates strong demand. Alphabet disclosed about USD 106 billion in contracted cloud revenue, with several deals exceeding USD 1 billion signed in the first half of 2025. This level of volume shows that big enterprises are integrating GCP into their long-term budgets.

However, these contracts need to be delivered efficiently, and capital expenditures are substantial. Efficiency is the key factor. If margins can stay above 20% while Alphabet invests billions into data centers and AI infrastructure, Cloud will become a consistent earnings contributor.

If cost discipline falters, the leverage could quickly unwind. The upside is real, but it all comes down to execution.

Next quarter, I will be closely watching whether operating margins continue to grow. That will be a signal that the model is scaling correctly.

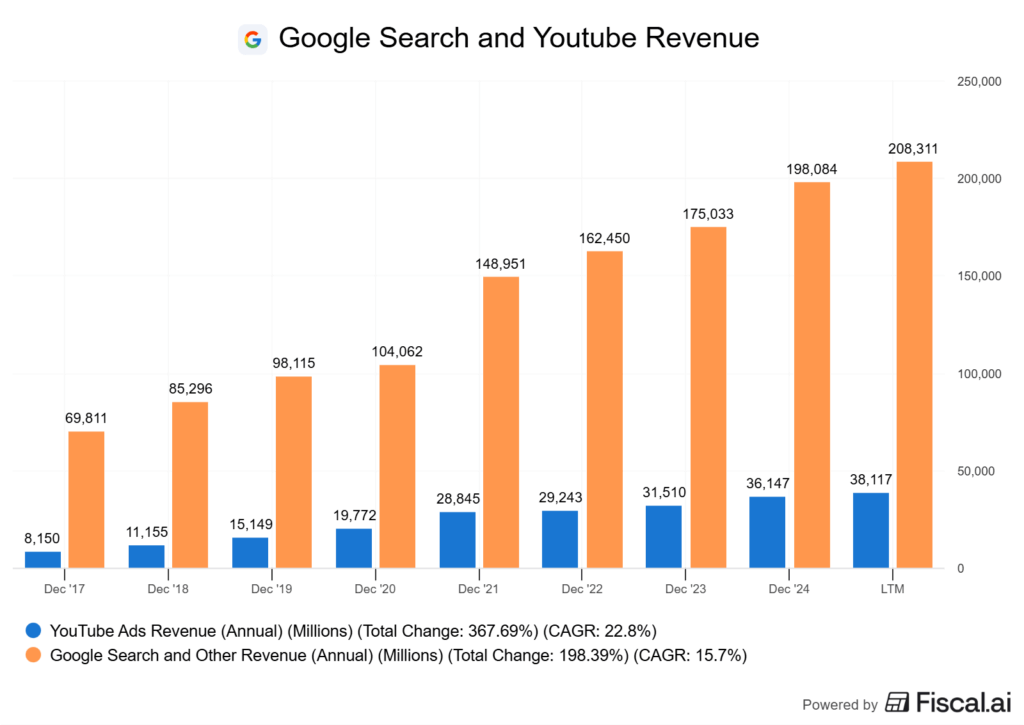

YouTube and Search Continue to Generate Cash, Even as AI Competition Intensifies

Search and YouTube still fund everything else at Alphabet. In Q2 2025, Search and Other revenues reached about USD 52.4 billion, up 12% year over year. YouTube ads grew another 13%, demonstrating that advertisers still view it as a must-buy channel despite the rise of TikTok.

One factor fueling YouTube Ads is the ability to develop ads via AI, which reduces the annoyance of creating video ads. Google's money-making strategy here is straightforward: ads tied to intent. On Search, this involves sponsored results when people look for products. On YouTube, it includes pre-rolls and targeted video ads. Both platforms use AI to refine targeting, which improves engagement and keeps cost-per-click steady, encouraging more advertisers to return.

AI Overviews and the new AI Mode are wild cards. Alphabet reports that AI Overviews already reaches 1.5 billion users monthly and could scale to 4 billion by year-end. While I don't find them particularly valuable right now, if any company can turn them into profitable tools, it's Alphabet.

This massive reach keeps search queries within Google's ecosystem instead of leaking to competitors like Microsoft's Copilot or Meta's Llama-driven tools. The risk is that if AI answers reduce ad clicks, the monetization model could become unstable unless adaptations occur.

Competition isn't standing still. Microsoft is embedding AI into Office, where enterprise adoption is sticky. Meta is pushing AI into its social platforms, where time spent is extensive.

Google's advantage lies in integration. Search, YouTube, and Workspace are all tied into Gemini, creating network effects, but only if regulators allow it.

I'll be monitoring ad monetization rates within AI Overviews over the next year. If they launch them and keep them close to traditional search, Google maintains its cash machine. If not, the AI pivot looks less sturdy.

Alphabet’s AI Bets Are No Longer Just Hype—Real Products Are Rolling Out

Alphabet has transitioned from promises to real rollouts. The Gemini app now has about 450 million users, while AI Overviews in Google Search reach an estimated 1.5 billion users. That's not just a pilot; it's mass adoption on a scale few companies can match.

AI Mode, available in the U.S. and India, already has over 100 million monthly active users. People aren't just testing it; they're sticking with it. Sustained usage is more important than flashy launches.

Agentic AI is another key factor. These systems handle tasks end-to-end without constant prompts. If Alphabet can make this reliable at scale, it could reshape how people and businesses interact with its ecosystem.

The risk is that deployments might still be too narrow to move revenue quickly. The product rollout goes beyond search. Google Cloud is layering generative AI into enterprise tools, and YouTube is experimenting with AI-driven editing and recommendations.

Each move ties back to Alphabet's core model: more engagement means more monetizable surface area. Billions of users are already exposed to AI features. The risk is that it doesn't scale cleanly in every market Alphabet touches.

I'll be watching how user adoption of AI Overviews and Gemini translates into higher ad yield and Cloud revenue next quarter. That will show if this is more than just engagement at scale.

Antitrust Headwinds Ease After Recent Resolution, Clearing a Path Forward

The Department of Justice’s long-running antitrust lawsuit against Google Search finally reached a resolution. The judge did not force a breakup, which was a relief for investors, and instead imposed targeted remedies. This outcome is a huge win for Google, reducing structural risk while acknowledging its monopoly ruling.

The court barred Google from paying for exclusive search placement deals but allowed default arrangements to continue. That keeps the Apple partnership intact, worth about USD 20 billion annually.

The remedies also require Google to share some search data with competitors and stop tying certain products together. On paper, this opens the door for rivals like Microsoft and DuckDuckGo. In reality, the impact seems minimal. These firms still face scale disadvantages, and the rise of generative AI has already created more competition than regulators could engineer.

Investor confidence increased after the ruling, and Alphabet’s shares reflected that relief. I see this as markets pricing in stability, not sudden growth.

The risk is that remedies only work if regulators enforce them consistently. If Google pushes too hard on default deals or data control, regulators could revisit structural options. But for now, the regulatory resolution gives Alphabet much-needed breathing space.

Alphabet’s Massive Buybacks and Cash Position Offer Shareholder-Friendly Stability With Large Upside

Alphabet’s capital return strategy is difficult to ignore. In 2024, the company announced a $31.4 billion share buyback. I expect amplified buybacks to continue in 2025.

Moves like this don’t just shrink the share count. They also send a clear message: management sees real value in its own stock.

The real backbone here is free cash flow. Alphabet generated USD 5.3 billion in free cash flow last quarter. Trailing twelve-month levels hit USD 66.7 billion. That kind of consistency suggests the advertising and cloud engines are still generating cash at scale, allowing it to expand its AI offerings without relying on debt.

For investors, the durability of that cash flow matters more than any one quarter. Cash reserves remain another point of strength. Alphabet ended the period with roughly USD 95 billion in cash. That’s not just idle money; it gives the company room to keep investing in AI, fund acquisitions, and still return capital without stretching its balance sheet.

Not many peers can balance growth spending and capital returns at this scale. The mix leans heavily toward buybacks, which tend to be more tax-efficient than dividends for many investors. However, I expect the dividend to continue growing.

However, the tilt towards buybacks makes me believe management wants the flexibility to avoid a large fixed-payment in terms of a dividend. If margins weaken or ad spend slows, the cash engine could lose some of its buffer, and raising the dividend too much could slow them down.

But right now, Alphabet’s financial strength allows it to reward shareholders while still funding its growth bets. I view it as one of the best tech stocks on the planet. Yes, right up there with the likes of NVIDIA and Apple.

{kind=link}

Post a Comment for "Alphabet's Unstoppable Rise – Here's the Reason"

Post a Comment