Universal Health Q2 Earnings Surpass Expectations with Rise in Acute Care Admissions

Strong Financial Performance in Q2 2025

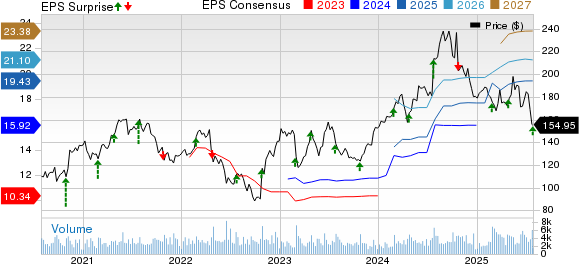

Universal Health Services, Inc. (UHS) reported strong second-quarter 2025 results, with adjusted earnings per share (EPS) reaching $5.35. This exceeded the Zacks Consensus Estimate by 10.3%, marking a significant improvement over the previous year’s performance. The company’s bottom line increased by 24.1% year over year, reflecting robust growth across its operations.

Net revenues for the quarter climbed to nearly $4.3 billion, representing a 9.6% increase compared to the same period in 2024. This result surpassed the consensus estimate by 1.5%, demonstrating the company's ability to outperform market expectations.

The positive results were driven by continued growth in admissions at UHS’s acute care facilities and behavioral health care services. These segments contributed significantly to the overall revenue increase. However, higher operating expenses partially offset some of the gains, highlighting the challenges the company faces in managing costs while maintaining profitability.

Operational Highlights

Adjusted EBITDA, net of non-controlling interest (NCI), reached $642.9 million in the second quarter, an increase of 11.1% compared to the same period last year. This figure also exceeded the company’s internal estimate of $602.8 million, showcasing strong operational performance.

Total operating costs rose by 9% year over year, reaching $3.8 billion. This increase was primarily due to higher salaries, wages, benefits, supplies, and other operating expenses. Despite this, the company managed to maintain its financial momentum through improved revenue generation.

Segmental Performance

Acute Care Hospital Services

In the acute care segment, adjusted admissions, which account for outpatient activity, increased by 2% on a same-facility basis. Adjusted patient days grew by 1.1% year over year. Net revenues from acute care services advanced by 7.9% on a same-facility basis, indicating steady demand for hospital services.

Behavioral Health Care Services

The behavioral health care segment saw a modest increase in adjusted admissions, rising by 0.4% on a same-facility basis. Adjusted patient days also increased by 1.2% year over year. Net revenues from this segment grew by 8.9% on a same-facility basis, reflecting continued demand for mental health and substance abuse treatment services.

Financial Position as of June 30, 2025

As of the end of the second quarter, UHS had cash and cash equivalents of $137.6 million, up from $126 million at the end of 2024. The company maintained a revolving credit facility of $1.3 billion, with $1.08 billion in available borrowing capacity after accounting for outstanding borrowings and letters of credit.

Total assets stood at $15 billion, an increase from $14.5 billion at the end of 2024. Long-term debt reached $4.5 billion, representing a 1.7% increase from the previous year. Current maturities of long-term debt totaled $40.9 million.

Total equity increased to $7.1 billion, up from $6.7 billion at the end of 2024. Cash flows from operations declined by 19.2% to $549 million in the second quarter, reflecting higher operating costs and capital expenditures.

Share Repurchase Activity

UHS repurchased shares worth $150.8 million during the quarter. As of June 30, 2025, the company had approximately $492.9 million remaining in its share repurchase authorization, providing flexibility for future buybacks.

2025 Guidance

Management updated its full-year guidance for 2025, raising the expected range for net revenues to between $17.096 billion and $17.312 billion. Previously, the range was set at $17.020 billion to $17.364 billion.

Adjusted EBITDA, net of NCI, is now expected to be in the range of $2.458 billion to $2.543 billion, compared to the earlier forecast of $2.357 billion to $2.484 billion. EPS is projected to be between $20 and $21, up from the previous range of $18.45 to $19.95.

Depreciation and amortization expenses are estimated at $639.6 million, with interest expenses expected to be around $150.3 million. Capital expenditures are anticipated to fall between $850 million and $1 billion. The provision for income taxes is expected to be in the range of $376.81 million to $407.31 million.

Zacks Rank and Key Picks

UHS currently holds a Zacks Rank of #3 (Hold), indicating a neutral outlook. In the medical sector, several stocks have a stronger rating:

- West Pharmaceutical Services Inc (WST) – Zacks Rank #1 (Strong Buy)

- Fresenius Medical Care AG & Co. (FMS) – Zacks Rank #1 (Strong Buy)

- Doximity, Inc. (DOCS) – Zacks Rank #1 (Strong Buy)

These companies have shown consistent earnings beat performance and positive analyst sentiment. For example, West Pharmaceutical Services has seen four upward revisions to its earnings estimate in the past seven days, with an average earnings surprise of 16.8% over the last four quarters. Its current-year revenue estimate stands at $3 billion, reflecting 4.6% growth year over year.

Fresenius Medical Care has also seen four upward revisions to its earnings estimate in the past 60 days, with an average earnings surprise of 6.6%. Its current-year revenue estimate is $22 billion, signaling 5.2% growth.

Doximity has one upward revision to its earnings estimate in the past 60 days, with an average earnings surprise of 29.9% over the last four quarters. Its current-year revenue estimate is $625.7 million, indicating 9.7% growth.

{kind=link}

Post a Comment for "Universal Health Q2 Earnings Surpass Expectations with Rise in Acute Care Admissions"

Post a Comment