UnitedHealth Q2 Earnings Fall Short Amid Rising Medical Costs

UnitedHealth Group's Second-Quarter Performance in 2025

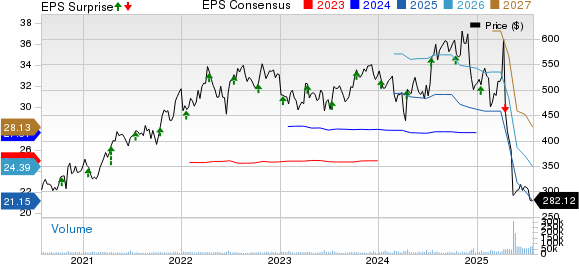

UnitedHealth Group Inc. (UNH) reported second-quarter 2025 adjusted earnings per share (EPS) of $4.08, which fell short of the Zacks Consensus Estimate of $4.84. The bottom line saw a significant decline of 40% compared to the same period last year. Despite this, revenues increased by 12.9% year over year to $111.6 billion, slightly exceeding the consensus mark by 0.1%.

The weak quarterly earnings were influenced by higher medical costs, although these were partially offset by growth in domestic commercial membership and strong performance from Optum Rx.

Business Performance Overview

In the second quarter, UnitedHealth’s premium income reached $87.9 billion, up from $76.9 billion in the same period last year and surpassing the consensus estimate by 0.8%. However, the company’s medical care ratio (MCR) rose to 89.4%, an increase of 430 basis points from the previous year. This was higher than both the Zacks Consensus Estimate of 88.6% and the company’s own estimate of 87%. The rise in MCR was attributed to reductions in Medicare funding and medical cost trends that outpaced pricing trends. Medical costs for the quarter totaled $78.6 billion, up from $65.5 billion in the prior year.

Total operating costs for the quarter surged by 17% year over year to $106.5 billion, driven by higher medical costs and product expenses. This figure exceeded the model estimate of $103.8 billion. However, the operating cost ratio improved to 12.3% from 13.3% in 2024, thanks to technological efficiencies and Part D programs.

UnitedHealth’s operating earnings declined by 34.6% to $5.2 billion in the second quarter, with the net margin dropping 120 basis points to 3.1% from the previous year.

Performance of Key Business Platforms

UnitedHealthcare, the health benefits segment, saw revenue increase by 17% year over year to $86.1 billion, driven by growth in domestic commercial membership. This surpassed the Zacks Consensus Estimate of $84.8 billion. However, operating earnings dropped to $2.1 billion from $4 billion, with the operating margin declining by 300 basis points to 2.4%.

Optum, the other major business line, generated $67.2 billion in revenue, up 6.8% year over year due to contributions from Optum Rx. However, this fell slightly below the consensus estimate of $67.5 billion. Operating earnings for Optum declined to $3.1 billion from $3.9 billion, with the operating margin decreasing by 160 basis points to 4.6%.

Membership and Financial Position

As of June 30, 2025, UnitedHealthcare served 50.1 million people, reflecting a 2.1% year-over-year increase due to growth in self-funded commercial benefits. However, this fell short of the Zacks Consensus Estimate of 50.3 million and the company’s own forecast of 50.2 million.

Financially, UnitedHealth ended the second quarter with $32 billion in cash and short-term investments, up from $29.1 billion at the end of 2024. Total assets reached $308.6 billion, compared to $298.3 billion at the end of 2024. Long-term debt, less current maturities, stood at $73.5 billion, an increase from $72.4 billion as of December 31, 2024.

Operating cash flows for the quarter surged to $7.2 billion, up from $2.2 billion in the same period last year. Shareholders received $4.5 billion in dividends and share repurchases during the quarter, with the company raising its quarterly dividend rate by 5% in June.

Outlook for 2025

Management now projects adjusted net EPS for 2025 to be at least $16, down from the previous guidance range of $26 to $26.50. Net earnings are expected to reach at least $14.65 billion, up from $14.4 billion in 2024. Revenue is projected between $445.5 billion and $448 billion in 2025, compared to $400.3 billion in 2024. Operating cash flows are expected to decrease to $16 billion from $24.2 billion in 2024.

Zacks Rank and Market Outlook

UnitedHealth currently carries a Zacks Rank of #4 (Sell). In contrast, several stocks in the medical sector have a Zacks Rank of #1 (Strong Buy), including West Pharmaceutical Services Inc. (WST), Fresenius Medical Care AG & Co. (FMS), and Doximity, Inc. (DOCS).

West Pharmaceutical Services has seen four upward revisions to its earnings estimate in the past seven days, with the current-year estimate at $6.61 per share. The company has consistently beaten earnings estimates in the past four quarters, with an average surprise of 16.8%.

Fresenius Medical Care has also seen positive revisions, with the current-year earnings estimate at $2.22 per share. The company has beaten estimates in three of the past four quarters, with an average surprise of 6.6%.

Doximity has one upward revision in the past 60 days, with the current-year earnings estimate at $1.46 per share. The company has met or exceeded expectations in all four of the past quarters, with an average surprise of 29.9%.

{kind=link}

Post a Comment for "UnitedHealth Q2 Earnings Fall Short Amid Rising Medical Costs"

Post a Comment